Smurfing Vs Structuring: Money Laundering & Banking Guide

⚡Key Takeaways

Structuring vs Smurfing in Financial Crimes

Structuring and Smurfing are the two practices that have emerged as prevalent tactics employed by individuals and criminal organizations. While these terms are often used interchangeably, they represent distinct methods with varying levels of complexity and legal implications.[1]

Smurfing Vs Structuring Comparison – Image By Cellbunq

As businesses navigate the ever-evolving landscape of financial regulations, understanding the nuances between these two practices is crucial for maintaining compliance and safeguarding against potential risks.

Structuring

Structuring, also known as micro-structuring or smurfing in certain contexts, is a deliberate tactic employed by individuals or organizations to circumvent Anti-Money Laundering (AML) and Counter-Terrorist Financing (CTF) regulations.[2]

It involves the intentional division of large sums of money into smaller transactions, each falling below the reporting threshold set by financial institutions and regulatory bodies.

The primary objective of structuring is to evade detection and reporting requirements that apply to substantial financial transactions. By making numerous small deposits or withdrawals, individuals aim to conceal the true source, purpose, or destination of the funds, effectively flying under the radar of financial institutions and regulatory authorities.

To illustrate the concept of structuring, consider the following scenarios:

- An individual has $50,000 in cash, and instead of depositing the entire amount in one transaction, they make ten separate deposits of $5,000 each to avoid triggering a Currency Transaction Report (CTR) or a Suspicious Activity Report (SAR).

- A business owner regularly receives cash payments and intentionally deposits amounts just below the reporting threshold to circumvent scrutiny from financial institutions.

Even if the money was legitimately earned, the deliberate attempt to evade reporting obligations is considered a criminal offense, carrying significant legal consequences.[3]

Smurfing

Smurfing, while sharing similarities with structuring, is a more sophisticated scheme that involves a network of individuals commonly referred to as “smurfs.” These low-level financial criminals are recruited by the primary offender to move illegally obtained funds into the legitimate financial system.

This method significantly complicates the trail of illicit funds, making it challenging for financial institutions and law enforcement agencies to establish a link between the smurfs, deposits, and accounts involved.[4]

Consider the following scenario:

- A criminal organization has obtained a substantial amount of cash through illegal means, such as drug trafficking or fraud.

- The organization recruits several individuals, known as “smurfs,” to assist in laundering illicit funds.

- Each smurf is given a portion of the cash and instructed to deposit it into multiple bank accounts across various financial institutions, using different identities or aliases.

- The smurfs may also engage in other tactics, such as purchasing valuable assets like real estate or artwork, to further obscure the trail of the illegal funds.

By employing this intricate network of smurfs and utilizing various methods to conceal the source of the funds, criminal organizations aim to integrate the illicit money into the legitimate financial system, making it appear as though it originated from legal sources.

Distinguishing Structuring from Smurfing

While smurfing and structuring share many similarities, such as breaking down large sums into smaller transactions, there are key distinctions between the two practices. The primary difference lies in their complexity and the nature of the network involved.

Structuring typically involves a single individual making multiple deposits or withdrawals just below the reporting threshold. On the other hand, smurfing is a more sophisticated operation that involves a network of “smurfs” making numerous deposits across various accounts, often using different identities or aliases.[5]

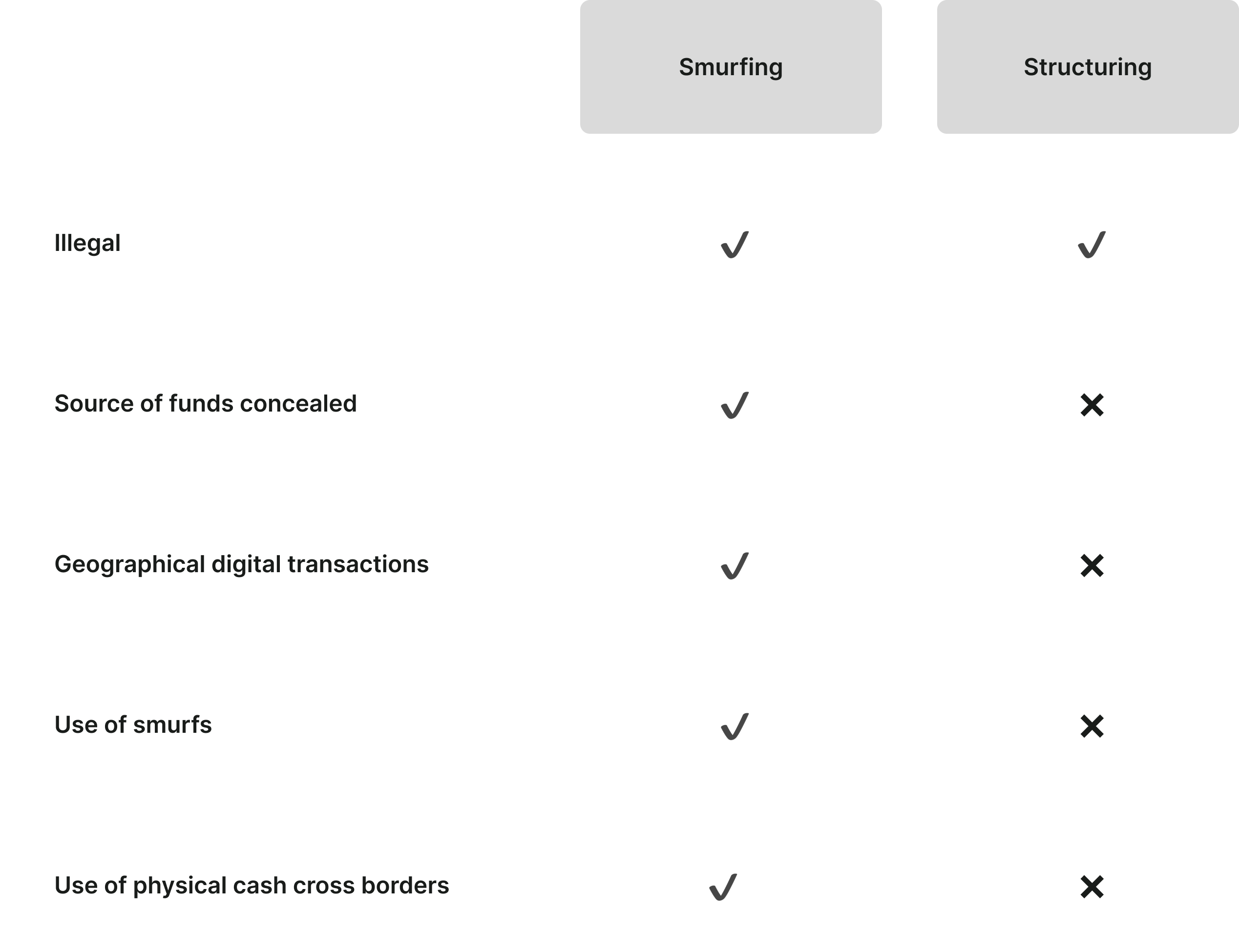

Here’s an overview of the key differences between structuring and smurfing:

| Aspect | Structuring | Smurfing |

|---|---|---|

| Legality | Illegal | Illegal |

| Use of “Smurfs” | No | Yes |

| Source of Funds | Often concealed but may be legal | Illegally obtained |

| Money Movement | Transactions within a single jurisdiction | Transactions across multiple jurisdictions |

| Complexity | Relatively simple | Highly complex |

| Network Involvement | Single individual | Network of individuals (“smurfs”) |

It’s important to note that while both practices are illegal, smurfing is typically associated with more severe criminal activities, such as drug trafficking, terrorism financing, and large-scale money laundering operations.

Legal Implications and Preventative Measures

To mitigate the risks associated with smurfing and structuring, financial institutions and businesses must adhere to stringent legal and regulatory frameworks designed to combat these illicit activities:

- Regulatory Compliance:

- Implement robust Know Your Customer (KYC) procedures to verify customer identities and assess their risk profiles.

- Adhere to AML regulations which mandate the filing of Currency Transaction Reports (CTRs) and Suspicious Activity Reports (SARs) for transactions that meet certain thresholds or appear suspicious.

- Regularly conduct risk assessments to identify vulnerabilities in systems that might be exploited for smurfing or structuring.

- Technological Solutions:

- Utilize advanced anti-money laundering tools and detection algorithms, including AI-powered identity verification systems, to monitor and analyze transactions for potential risks.

- Employ digital solutions to integrate global intelligence and automate sanctions screening, enhancing the detection of smurfing and structuring activities.

- Legal Consequences:

- Understand that engaging in smurfing or structuring is illegal and can result in severe penalties, including imprisonment of up to 20 years for money laundering and up to five years for structuring.

- Financial institutions face the obligation to report any suspicious activities, and failure to comply can lead to significant legal and reputational risks.

These measures are critical in maintaining the integrity of financial systems and protecting businesses from the potential legal repercussions associated with these criminal practices.[6]

Identifying and mitigating the risks of structuring and smurfing is critical for preserving a firm’s reputation and maintaining compliance with regulatory requirements. AML professionals must stay abreast of the common methods employed by criminals and be vigilant in spotting red flag indicators.

Common Red Flags for Structuring and Smurfing

- Multiple cash deposits or withdrawals just below the reporting threshold.

- Frequent round-number transactions.

- Sudden changes in account activity or transaction patterns.

- Use of multiple accounts or branches for transactions.

- Lack of reasonable explanation for the source of funds.

- Inconsistencies between stated business activities and financial transactions.

Compliance teams should be trained to recognize these and other potential indicators of structuring and smurfing. Regular staff training and awareness programs can equip employees with the knowledge and skills necessary to identify and report suspicious activities promptly.[7]

References

- financialcrimeacademy – Money laundering exposed: The Art of Structuring unveiled. Financial Crime Academy. https://financialcrimeacademy.org/structuring-in-money-laundering/

- u4 – The impact of anti-money laundering and counter terrorist financing regulations on civic space and human rights. U4 Anti-Corruption Resource Centre. https://www.u4.no/publications/the-impact-of-anti-money-laundering-and-counter-terrorist-financing-regulations-on-civic-space-and-human-rights

- imf – Anti-Money laundering and combating the financing of terrorism. IMF. https://www.imf.org/en/Topics/Financial-Integrity/amlcft

- investopedia – What is a smurf and how does smurfing work? Investopedia. https://www.investopedia.com/terms/s/smurf.asp#toc-what-is-a-smurf

- investopedia – How Big Is America’s Underground Economy? Investopedia. https://www.investopedia.com/articles/markets/032916/how-big-underground-economy-america.asp

- fincen – Suspicious Activity Reporting (Structuring) | FinCEN.gov. https://www.fincen.gov/resources/statutes-regulations/administrative-rulings/suspicious-activity-reporting-structuring

- austrac – Detect and report cuckoo smurfing – https://www.austrac.gov.au/business/how-comply-guidance-and-resources/guidance-resources/cuckoo-smurfing

Good job! Please give your positive feedback

How could we improve this post? Please Help us.

Astrid Johansson

[Trainee] Astrid is one of Cellbunq’s latest add-ons to the team, she is currently undergoing a bachelor's degree in Artificial Intelligence at the Stockholm University of Technology (SIT). Connect With Her LinkedIn